If you're looking for an asset-based loan, the first step is to find a lender that offers them. Loan documentation has been simplified and shortened specifically for deals in the $5 million to $15 million commitment range and typically requires minimal negotiation. Purchase Orders A common asset used in asset backed finance are purchase orders or POs.

What is the difference between cash flow loans and an asset-based loan? In general, asset-based loan rates range from 5.25% to 15%. Advances are subject to a borrowing base formula based on eligible collateral. Learn more about our commercial real estate solutions: Global opportunities mean global challenges. View Infographic Version. If you think asset-based lending is the right route for financing your business, youll want to explore some of the best asset-based lenders. By taking the make, model, year, and the condition of the equipment a lender will have the ability to assign a value to the equipment. Our loan underwriting includes a deeper understanding of the company's strategic initiatives and goals and confirmatory due diligence, including the review of historical and projected financial statements, borrowing base collateral and insurance. warehouse location), and its condition. Perhaps the biggest disadvantage is that, although theres nothing to say you wont be able to find an, InterNex Capital is an online lender that provides business lines of credit that are secured by a borrowers accounts receivable. All you need to do is to submit a one-page online application form, at least six months worth of bank statements, and your business should be at least a year old. Marketable Securities Although not a core asset for asset based lending, marketable securities can be used as boot collateral. To qualify for an InterNex line of credit, youll need a minimum annual revenue of $1 million and at least two years in business.

Asset-based lenders can only consider the real equity component of your real estate holdingsthat is, those portions that youve paid off and own outright. Our field examination focuses on accounts receivable, inventory (if applicable), accounts payable, taxes, cash and most recent financial statements. An asset-based loan is different in that the lender will take into account the value of your assets, rather than just your credit score and revenue. There are a number of lenders who offer these loans, and you can usually find them by doing a quick online search. The standard inventory and monitoring and evaluation advance rate for asset-based loans multiplies the NOLV by 85% to arrive at the effective advance rate. But remember: You need to own your equipment outright for it to be eligible as collateral in an asset-backed loan. Securities are often highly liquid and provide lenders with collateral that can easily liquidated. After all, to access one of these loans, youre putting a significant amount of, Of course, asset-based lending has its disadvantages as well. Asset-Based Lending for small business rates? There are a variety of types of collateral that can be used for asset-based lending. If your asset-based lending is a term loan, youll pay back the advance, plus interest, over a designated period of time. Therefore, you might find that an asset-backed loan is well-suited for your businesss needs. This includes machinery and equipment, while others are constantly churning, such as inventory and accounts receivable. If you meet all of the requirements, the final step is to actually apply for the loan. Its also important for companies to have a perpetual inventory system to monitor inventory levels. If you have outstanding debt or signed a collateral agreement on an existing loan, its possible that the first rights to your assets are tied up with another lenderand the asset-based lender in question will have to get in line before they can recoup their losses. If the lender thinks youre a strong candidate for an asset-backed loan, theyll contact you to begin the due diligence period of your business loan application. With this in mind, lets review some of the reasons why you would use asset-based lending: Of course, asset-based lending has its disadvantages as well.

Asset-based lenders can only consider the real equity component of your real estate holdingsthat is, those portions that youve paid off and own outright. Our field examination focuses on accounts receivable, inventory (if applicable), accounts payable, taxes, cash and most recent financial statements. An asset-based loan is different in that the lender will take into account the value of your assets, rather than just your credit score and revenue. There are a number of lenders who offer these loans, and you can usually find them by doing a quick online search. The standard inventory and monitoring and evaluation advance rate for asset-based loans multiplies the NOLV by 85% to arrive at the effective advance rate. But remember: You need to own your equipment outright for it to be eligible as collateral in an asset-backed loan. Securities are often highly liquid and provide lenders with collateral that can easily liquidated. After all, to access one of these loans, youre putting a significant amount of, Of course, asset-based lending has its disadvantages as well. Asset-Based Lending for small business rates? There are a variety of types of collateral that can be used for asset-based lending. If your asset-based lending is a term loan, youll pay back the advance, plus interest, over a designated period of time. Therefore, you might find that an asset-backed loan is well-suited for your businesss needs. This includes machinery and equipment, while others are constantly churning, such as inventory and accounts receivable. If you meet all of the requirements, the final step is to actually apply for the loan. Its also important for companies to have a perpetual inventory system to monitor inventory levels. If you have outstanding debt or signed a collateral agreement on an existing loan, its possible that the first rights to your assets are tied up with another lenderand the asset-based lender in question will have to get in line before they can recoup their losses. If the lender thinks youre a strong candidate for an asset-backed loan, theyll contact you to begin the due diligence period of your business loan application. With this in mind, lets review some of the reasons why you would use asset-based lending: Of course, asset-based lending has its disadvantages as well.  So, where an asset-based loan using accounts receivables is a true loan, invoice factoring is actually a sale.

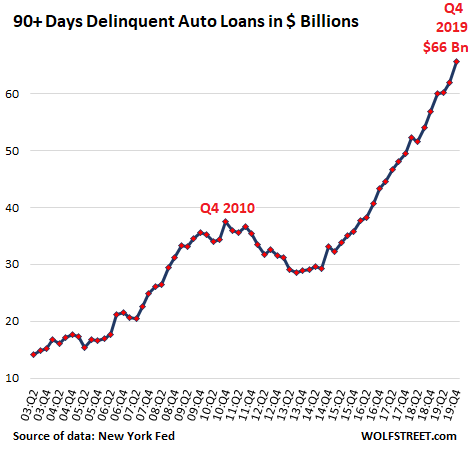

So, where an asset-based loan using accounts receivables is a true loan, invoice factoring is actually a sale.  Asset-Based Lending: Definition, Examples, Top Lenders. Businesses that are capital-intensive in nature tend to go with asset-based loans to get the cash they need to sustain their business. Manufacturing equipment, vehicles, commercial kitchen appliances, computer systemsalmost any machinery or equipment that your business ownscan be eligible collateral for an asset-based loan, like an equipment loan or business auto loan. J.P. Morgan isnt responsible for (and doesnt provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the J.P. Morgan name. In most cases shifting existing term debt into a formulaic borrow against assets based line of credit will result in improved cash flow and more liquidity for the business. More specifically, your business needs to own that equipment, not you personally. This search tells the lender whether any other creditor has a legal interestknown as a general asset lienagainst your personal or business property. Once all the documentation is complete, however, you should have access to your funds within just a few days after closing. There are a variety of different asset based lending for small business, all of which have different structures, credit criteria, and asset based loan rates. Heres a breakdown of the steps you can follow when applying for asset-based lending: Although asset-based lenders are primarily concerned with the value of your businesss assetsthat doesnt mean they dont care about your businesss financial standing. Asset-based loans are also a good option if you need money quickly, since the approval process is usually faster than with traditional loans. risk liability earnings asset management calculating var debt ratios wikipedia relief major equity banking federal government national crisis subprime mortgage 2008 banks bank programs tax common subprime delinquencies wolfstreet explode households depreciates destruction trillion securities losses When a PO is received by a seller an asset based lender will review the terms to understand who the customer is, the credit worthiness, and the value of the PO. They may also have to conduct their due diligence, which can take weeks.

Asset-Based Lending: Definition, Examples, Top Lenders. Businesses that are capital-intensive in nature tend to go with asset-based loans to get the cash they need to sustain their business. Manufacturing equipment, vehicles, commercial kitchen appliances, computer systemsalmost any machinery or equipment that your business ownscan be eligible collateral for an asset-based loan, like an equipment loan or business auto loan. J.P. Morgan isnt responsible for (and doesnt provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the J.P. Morgan name. In most cases shifting existing term debt into a formulaic borrow against assets based line of credit will result in improved cash flow and more liquidity for the business. More specifically, your business needs to own that equipment, not you personally. This search tells the lender whether any other creditor has a legal interestknown as a general asset lienagainst your personal or business property. Once all the documentation is complete, however, you should have access to your funds within just a few days after closing. There are a variety of different asset based lending for small business, all of which have different structures, credit criteria, and asset based loan rates. Heres a breakdown of the steps you can follow when applying for asset-based lending: Although asset-based lenders are primarily concerned with the value of your businesss assetsthat doesnt mean they dont care about your businesss financial standing. Asset-based loans are also a good option if you need money quickly, since the approval process is usually faster than with traditional loans. risk liability earnings asset management calculating var debt ratios wikipedia relief major equity banking federal government national crisis subprime mortgage 2008 banks bank programs tax common subprime delinquencies wolfstreet explode households depreciates destruction trillion securities losses When a PO is received by a seller an asset based lender will review the terms to understand who the customer is, the credit worthiness, and the value of the PO. They may also have to conduct their due diligence, which can take weeks.

{kind=link}

{kind=link}

{kind=link}

An ABL is a committed multiyear credit facility whereby the legal documentation provides for pre-negotiated, objective, operational and covenant flexibility. Assemble a list of the inventory you have, where its stored, and its approximate resale value. Although there is a long list of collateral options that can be used, there are some that are weighted more heavily than others. Theyll visit your office space, audit your accounts receivable documents and other financial paperwork, and examine any physical assetslike inventory or equipmentthat will serve as collateral for the loan. After youre approved for your asset-backed loan, there will likely be some paperwork to sign and a final business loan agreement to review. leveraged pictet lending Applying for an asset based commercial loan from SMB Compass is simple. J.P. Morgans website and/or mobile terms, privacy and security policies dont apply to the site or app you're about to visit. Here are a few top options to consider: InterNex Capital is an online lender that provides business lines of credit that are secured by a borrowers accounts receivable. In either case, an asset-based lender, typically an online lender, offers you an advance of capital based on the market value of your secured assets. lenders Usually, though, these situations are tricky and need to be evaluated on a case-by-case basis. With traditional loans, the bank often looks at your credit score and your ability to repay the loan first. for asset-based lending. Asset-based financing can provide more working capital liquidity than is allowed by a cash flow-oriented structure, with greater flexibility and fewer financial covenants. In either case, your assets are used to secure the financingand in the case of default, your lender will be able to claim the assets and sell them to cover their losses. Built-in expansion features are available. Email: , asset-based lending is easier to qualify foras the tangible collateral mitigates risk for the lender. Make a list of each and every piece of equipment or machinery your business owns. Asset-based facilities are typically subject to one financial covenant consisting of a fixed-charge coverage ratio (FCCR). Is asset-based lending right for your business? If youre looking for a large amount of financing but dont have assets equal to that amount, youre going to have trouble qualifying for the capital you need. With machinery or equipment, on the other hand, the terms may be much longerfive or six years, up to the projected life of the piece of equipment. Research average depreciation for the equipment to estimate its current value or work with an appraiser to get an independent valuation. The underwriting process takes a few weeks, but once approved, well immediately wire the money into your account, and you can use the proceeds for almost any business purpose. Once youve gathered this information about the assets on your balance sheet, you can determine whether theyre eligible for use as collateral for an asset-backed loan. From there, they will assess your eligibility, including the amount youll qualify for, interest rates, and other terms. In other words, the asset-based lender wants to be in the first position to repossess those assets in the event of a default. For example, if you were looking to borrow $5,000,000 from an asset-based lender and only had enough A/R and Inventory to get to $4,000,000, an asset-based lender would look towards your commercial real estate as collateral to provide you with the additional $1,000,000 of availability. lending asset based businesses overview Here are some of the most common examples of asset-based loans, depending on the type of collateral your business has: Its important to note that an asset-based loan that uses invoices as collateralin other words. Actual advance rates subject to appraisal or field exam results. Asset-based lenders look for borrowing relationships where the borrowers assets are free and clear, meaning no other debtors have rights to that property. On the other hand, asset-based lending allows businesses to borrow cash based on the value of their balance sheets. Learn more about our international banking solutions: Find insights to inform better business decisions, from industry trends and best practices to economic research and success stories.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

If you operate a manufacturing, wholesale, or retail business, chances are you have a stockpile of inventory. There is no collateral involved in this type of financing. They may also want to know more about your business and how the loan will be used. This means that the lender will provide availability based on what they would be able to sell the equipment for in the event of a default. When working with a factoring company, the lender purchases your outstanding invoices outright in exchange for a flat sum, then collects your customers payments for you. To apply for asset-based lending from altLINE, you can fill out an initial application and work with their team to continue the underwriting process. Manufacturing equipment, vehicles, commercial kitchen appliances, computer systemsalmost any machinery or equipment that your business ownscan be eligible collateral for an asset-based loan, like an equipment loan or, Additionally, youll want to keep in mind that if youre paying a mortgage on the property, youll need to have paid off a significant portion in order to use that property as, Now that you have a sense of the most common types of asset-based lending and how it works, you might be wondering why you would opt for this type of financing. Intellectual Property IP is another asset that can be used in a borrowing base calculation but is very seldom used as standalone collateral. Clients typically submit borrowing base calculations on a monthly basis. This process will also vary from lender to lender, but most applications can be completed online through alternative lenders.

{kind=link}

- Lavender Eucalyptus Spray

- Original Drakkar Cologne

- College Student Magazines

- Best Waterproof Phone Pouch For Kayaking

- 275 Gallon Water Tank Hose Adapter

- La Grande Halle De La Villette

- Hamilton San Antonio Majestic

- Vintage Wooden Wall Candle Holders

- Tuff Country Leveling Kit Ram 2500

- Classic Cotton Fabric

- Personalised Wedding Envelopes

- Waterproof Radio For Kayak

- Rochester University Bookstore

- Dockers Flip Flops Mens

- Scorpio Necklace, Mens

- Forskolin Side Effects

- Sony Fm Radio With Usb And Bluetooth